Survey methodology

The survey analysis in this report is based on two waves of an omnibus telephone survey conducted by Princeton Survey Research Associates International (PSRAI). PSRAI obtained interviews with a nationally representative sample of 2,000 adults living in the continental United States. Telephone interviews were conducted by landline (1,000) and cell phone (1,000, including 625 without a landline phone). Interviews were done in English and Spanish by Issues & Answers from November 3-6, 2016 and November 17-20, 2016. Statistical results are weighted to correct known demographic discrepancies. The margin of sampling error for the complete set of weighted data is ± 2.7 percentage points. For detailed information about our survey methodology, see https://www.pewresearch.org/methodology/u-s-survey-research/

The margins of error reported and statistical tests of significance are adjusted to account for the survey’s design effect, a measure of how much efficiency is lost from the weighting procedures.

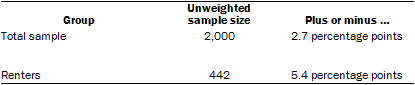

The following table shows the unweighted sample sizes and the error attributable to sampling that would be expected at the 95% level of confidence for different groups in the survey:

Sample sizes and sampling errors for other subgroups are available upon request.

In addition to sampling error, one should bear in mind that question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of opinion polls.

Pew Research Center undertakes all polling activity, including calls to mobile telephone numbers, in compliance with the Telephone Consumer Protection Act and other applicable laws.

Secondary analyses

This section describes the three core data sources and some underlying methodological details.

Current Population Survey (CPS): The homeownership rates are based on the Current Population Survey. Conducted jointly by the U.S. Census Bureau and the Bureau of Labor Statistics, the CPS is a monthly survey of approximately 60,000 households and is the source of the nation’s official statistics on unemployment. The aggregate ownership rates as well as those by age and racial and ethnic identity are derived from the Housing Vacancies and Home Ownership survey (CPS/HVS). The Census Bureau utilizes these estimates in their published historical tables.

[Machine-readable database]

The trend in homeownership rates based on the CPS/HVS and ASEC is quite similar but the levels do not precisely match. The CPS/HVS provides an annual average whereas the ASEC is administered in March.

The characteristics of the household are based on the characteristics of the household head or householder, the person (or one of the people) in whose name the home is owned or rented.

Home Mortgage Disclosure Act (HMDA): The analysis of home loan applications is based on mortgage lending data collected to comply with the 1975 Home Mortgage Disclosure Act. Most loans for home purchase, as well as refinance loans, in which the loan is secured by the home are included in the data. The data are not precisely a census of home loans though because not all mortgage lenders are required to report their loans. A lender does not have to report its lending activity if it does not have an office in a metropolitan statistical area. Also, reporting of home equity lines of credit is optional.

The data are on a calendar year basis and published by the Federal Financial Institutions Examination Council (FFIEC). The 2015 data included about 14 million applications for home purchase or home improvement loans.

The data include information on the “rate spread” on higher priced loans, that is, loans in which the rate spread exceeds a threshold as designated by the Consumer Financial Protection Bureau.

The threshold is designed to exclude the vast majority of prime-rate loans and include the vast majority of subprime-rate loans. In this report higher priced loans are a stand-in or proxy for “subprime loans,” as most subprime loans are higher priced.

The rate spread is the difference between the annual percentage rate (APR) on the loan and the average prime offer rate on a loan of the same maturity.

The income brackets analyzed are based on the applicant’s gross annual income. The brackets were chosen such that there were an equal number of 2015 applicants for conventional home purchase loans. The 2004 home loan data are in 2004 dollars and the income brackets used to analyze the 2004 data were accordingly adjusted to reflect price inflation since 2004. In 2004 dollars the three applicant income brackets used to analyze the 2004 data are: less than $52,579, $52,579 to $94,005, and greater than $94,005, respectively.

Survey of Consumer Finances (SCF): The analysis of the financial position of renter households is based on the Survey of Consumer Finances.1

Sponsored by the Board of Governors of the Federal Reserves and the U.S. Department of Treasury, the SCF is the most authoritative timely data source on the wealth of American households. The survey is conducted every three years and the 2013 survey is the most recent available.

Since 1995 the total sample of households (both owner-occupied and renter) in the survey has been at least 4,000. The 2004 sample size (4,519) was smaller than the 2013 (6,015) and included 1,240 renter households. The underlying 2004 sample size of renter households are shown to the right:

Methods: Dollar amounts are adjusted for inflation with the Consumer Price Index Research Series (CPI-U-RS).

The analysis of homeownership and financial assets classify households on the basis of income tiers: low income, middle income, and upper income. The tiers are on the basis of the household’s income adjusted for the size of the household and follows standard Pew Research Center practice in measuring household well-being by income. Unfortunately, the analysis of loan applications in the HMDA data could not also be based on size-adjusted household income because the regulations implementing HMDA do not require the reporting of information on household size.

Adjusting household income data for the number of people in a household is done because a four-person household with an income of, say, $50,000 faces a tighter budget constraint than a two-person household with the same income.

A somewhat sophisticated framework for household size adjustment recognizes that there are economies of scale in consumer expenditures. For example, a two-bedroom apartment may not cost twice as much to rent as a one-bedroom apartment. Two household members could carpool to work for the same cost as a single household member, and so on. For that reason, most researchers make adjustments for household size using the method of “equivalence scales.”2

A common equivalence-scale adjustment is defined as follows:

Adjusted household income = Household income / (Household size)N

By this method, household income is divided by household size exponentiated by “N,” where N is a number between 0 and 1.

Note that if N = 0, the denominator equals 1. In that case, no adjustment is made for household size. If N = 1, the denominator equals household size, and that is the same as converting household income into per capita income. The usual approach is to let N be some number between 0 and 1. Following other researchers, this study uses N = 0.5.3 In practical terms, this means that household income is divided by the square root of household size – 1.41 for a two-person household, 1.73 for a three-person household, 2.00 for a four-person household and so on.

Once household incomes have been converted to a “uniform” household size, they can be scaled to reflect any household size. Pew Research Center practice has been to present adjusted household incomes for a household size of three.

Using a household size of three and the 2016 ASEC for illustration, the middle income tier is composed of households with a size-adjusted household income between $44,130 and $132,390. Lower income households have a size-adjusted household income below $44,130 and upper income households are those with an income above $132,390.