Today’s employment report indicated that the U.S. economy added 192,000 nonfarm payroll jobs in March, slightly below the revised gain for February and a bit below Wall Street expectations. That essentially continues the pattern in place since late 2010: steady, decent job growth but only enough to chip away at the yawning jobs hole opened by the Great Recession. Even now, there are still 437,000 fewer payroll jobs than there were in January 2008.

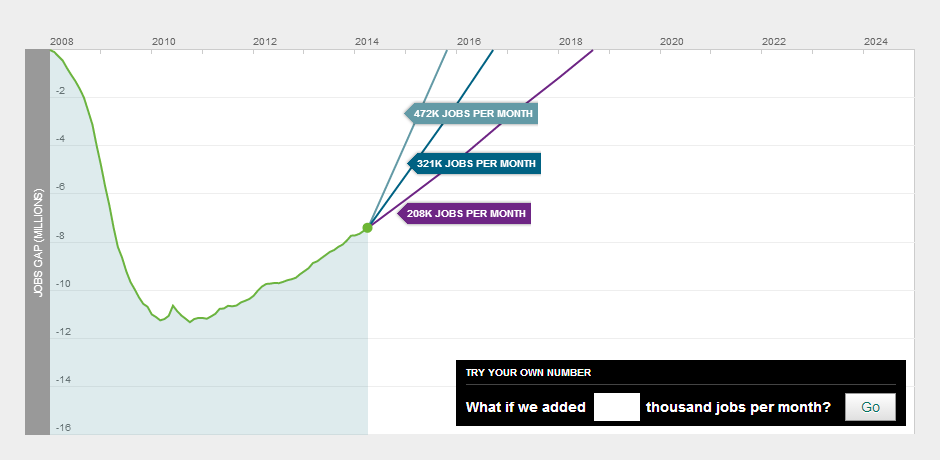

But that metric understates the jobs gap, as illustrated in the above chart from the Hamilton Project, an economic policy initiative of the Brookings Institution. (Clicking the chart will take you to an interactive graphic.) Because more people are entering the labor force each month, merely replacing all the jobs lost during the recession won’t bring employment back to its pre-crisis level.

Under the most optimistic scenario — the economy adds 472,000 jobs a month, the highest single-month rate in the 2000s — it would still take until October 2015 for employment to regain its pre-recession level. If the economy replicates its performance in 2005 (the best year since 2000) and adds about 208,000 jobs a month, it would take until September 2018. And if the economy continues to add jobs at the rate it has since late 2010 — an average of 182,000 a month — the employment gap won’t be closed till August 2019.